Don't Touch the Fed

This morning, President Trump nominated Kevin Warsh to succeed Jerome Powell as Chair of the Federal Reserve. The announcement caps months of public feuding between Trump and Powell, a DOJ criminal investigation into the sitting Fed Chair, and what might be the most aggressive pressure campaign a president has ever waged against the central bank.

Whether you think this is a good thing or a bad thing probably depends on how you feel about Trump. But the question underneath all of this is bigger than any single president or any single Fed Chair: should the person sitting in the Oval Office get to decide what happens to interest rates?

I think the answer is no. And I think the evidence for that answer is overwhelming. But this is not a simple story, and both sides have their reasons.

The Basics (For Those Who Need a Refresher)

The Federal Reserve has what economists call a "dual mandate": keep inflation low and stable, and support maximum employment. It does this mainly by adjusting interest rates. Raise them, and borrowing gets more expensive, which slows spending and cools inflation. Lower them, and money flows more freely, businesses expand, and hiring picks up.

The whole system is designed to keep these decisions at arm's length from whoever happens to be president. Fed governors serve 14-year terms. The chair can only be removed "for cause," which traditionally means serious misconduct, not just a policy disagreement. Congress set it up this way on purpose back in 1913 because it recognized a basic problem: presidents have elections to win, and elections reward short-term thinking. Cheap money feels great in the moment. The hangover comes later.

To put it in numbers: when the Fed keeps rates artificially low, it is essentially subsidizing borrowing today at the expense of price stability tomorrow. Every 1 percentage point drop in the federal funds rate makes roughly $360 billion in outstanding federal debt cheaper to service annually, which is why politicians love low rates, but it also tends to push inflation higher, which acts as a hidden tax on everyone holding dollars. The national debt currently sits north of $36 trillion. The incentive for any sitting president to lean on the Fed for cheaper borrowing costs is enormous, and it is getting bigger every year.

| Year | U.S. National Debt | Debt-to-GDP Ratio |

|---|---|---|

| 2020 | $27.7 trillion | ~129% |

| 2021 | $29.6 trillion | ~124% |

| 2022 | $30.8 trillion | ~123% |

| 2023 | $33.1 trillion | ~123% |

| 2024 | $34.4 trillion | ~122% |

| 2025 | $36.4 trillion | ~124% |

Source: U.S. Treasury Fiscal Data, FRED

The Historical Playbook: When Presidents Got Their Way

This tension between the White House and the Fed is as old as the Fed itself. But the most instructive period is probably the 1960s and 1970s.

President Lyndon Johnson reportedly shoved Fed Chair William McChesney Martin against a wall at his Texas ranch during an argument about interest rates. Richard Nixon took a different approach. He pressured Fed Chair Arthur Burns to keep rates low ahead of the 1972 election, and Burns, to his lasting discredit, largely went along with it. The economy got a short-term sugar rush, but the bill came due fast. Inflation spiraled through the rest of the decade, eventually peaking close to 15%.

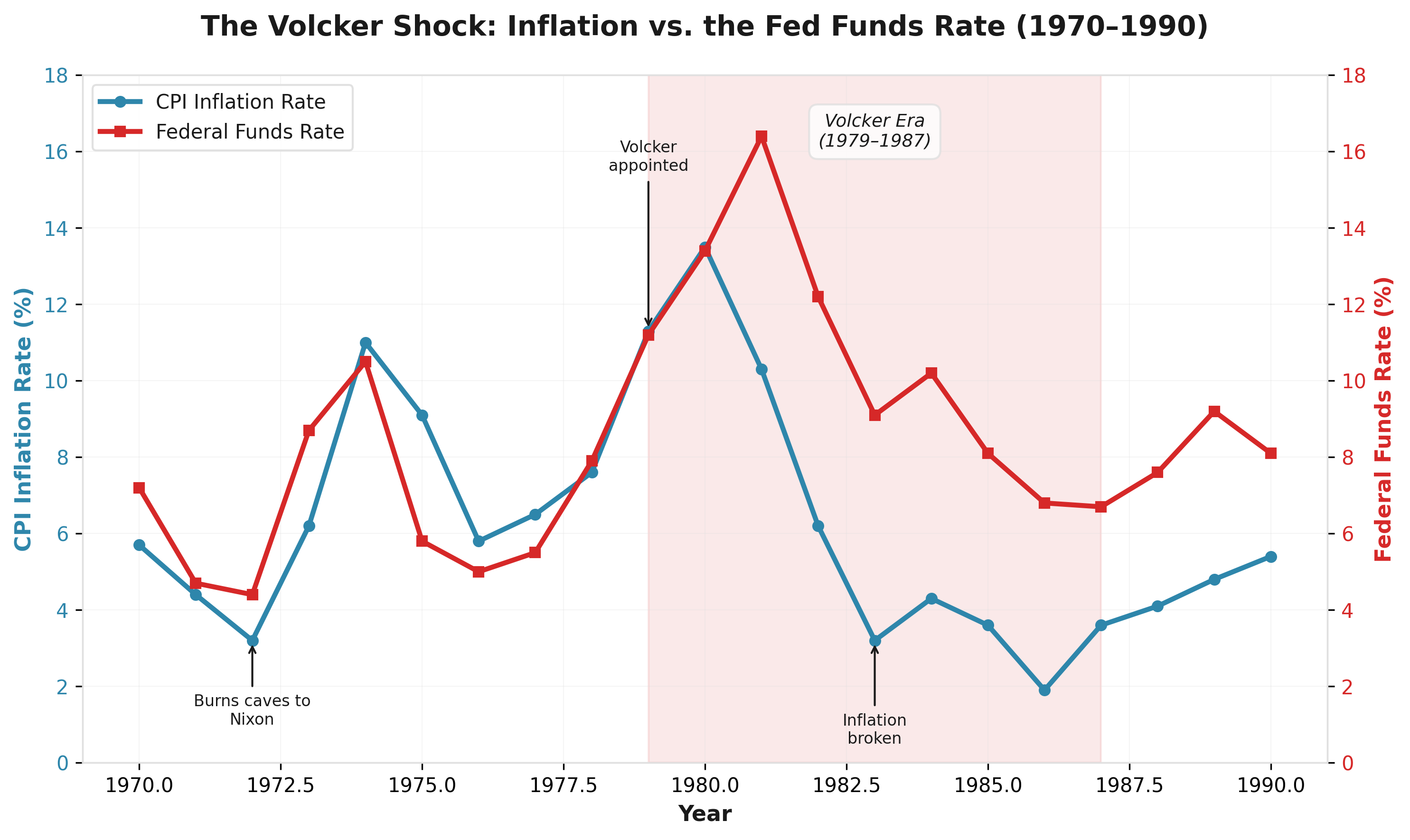

The numbers tell the story. When Burns caved to Nixon in 1972, inflation was running at a manageable 3.2%. By 1974, it had more than tripled to 11.0%. It briefly dipped in 1976 but then roared back, hitting 11.3% in 1979 and 13.5% in 1980. Over the full decade of the 1970s, cumulative inflation exceeded 100%, meaning the dollar lost more than half its purchasing power in ten years.

It took Paul Volcker, arguably the most consequential Fed Chair in American history, to clean up the mess. Volcker raised rates to nearly 20% in the early 1980s. The short-term pain was severe. Unemployment spiked to 10.8% by the end of 1982, the highest since the Great Depression. Farmers drove their tractors to the Fed building in Washington to protest. But Volcker held firm, and inflation broke. By 1983, it was back down to 3.2%. By 1986, it had fallen to 1.9%. The decades of relatively stable prices that followed, the period that defined the American economy through the 1990s and 2000s, were built directly on the foundation Volcker laid.

No president would have ever made that call. The political cost was too high. That is the strongest argument for Fed independence in a single sentence.

The Volcker Shock: How aggressive rate hikes in the early 1980s broke a decade of runaway inflation. Source: BLS, FRED

| Era | Inflation (Avg) | Fed Funds Rate (Avg) | Unemployment (Avg) | Outcome |

|---|---|---|---|---|

| Burns/Nixon (1970–1974) | 7.3% | 7.1% | 5.4% | Short-term boost, decade of stagflation |

| Late 1970s (1975–1979) | 8.1% | 7.1% | 7.0% | Inflation entrenched, dollar weakening |

| Volcker Shock (1980–1983) | 8.3% | 12.8% | 8.5% | Painful recession, but inflation broken |

| Post-Volcker (1984–1990) | 3.9% | 7.8% | 6.3% | Stable growth, foundation for 1990s boom |

Source: Bureau of Labor Statistics, FRED

Turkey: What Happens When the President Wins

If you want to see what it actually looks like when a head of state takes over monetary policy, Turkey is the case study. And it is not pretty.

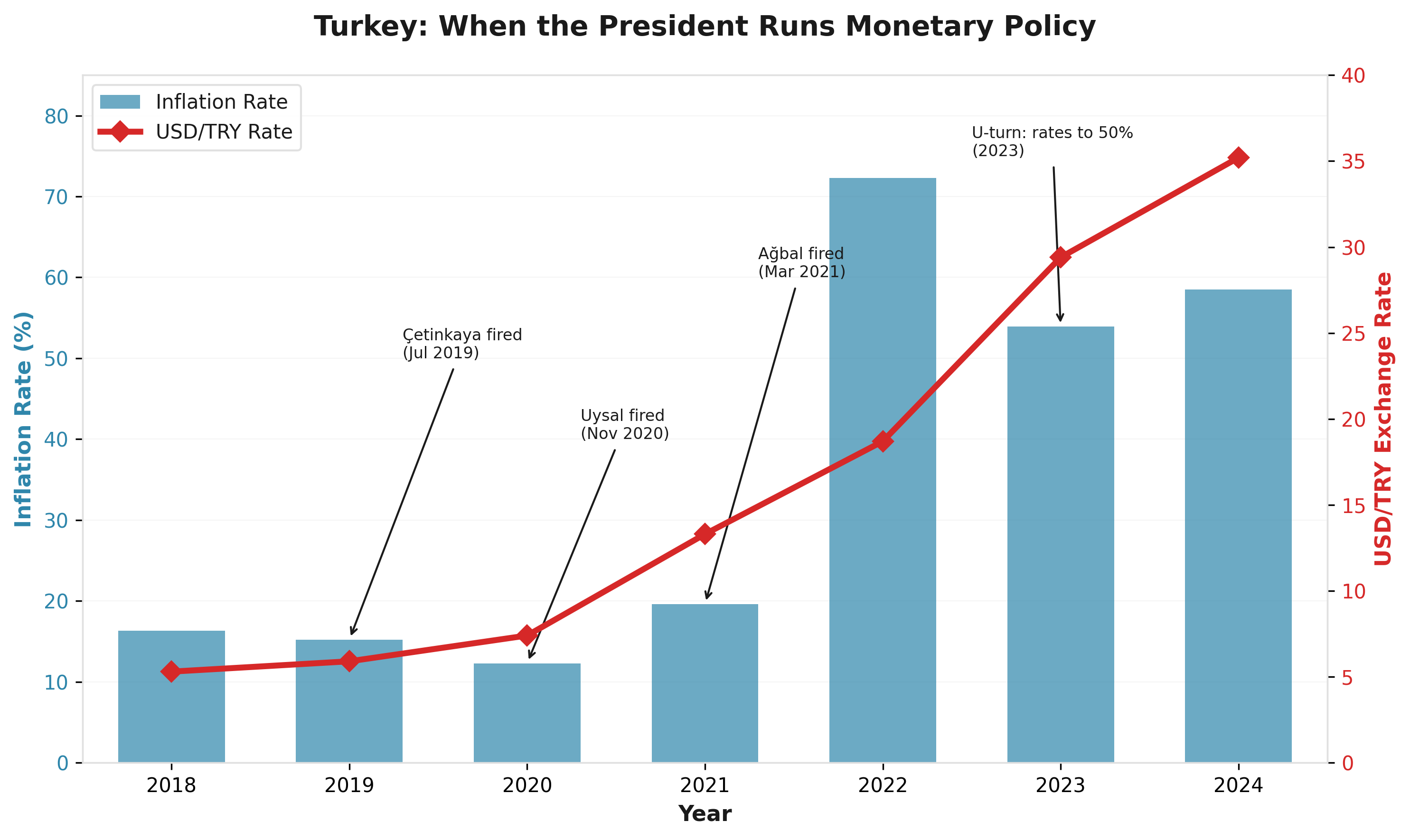

President Recep Tayyip Erdogan holds an unusual economic belief: he thinks high interest rates cause inflation. This is the opposite of what essentially every mainstream economist will tell you. Erdogan has acted on this belief aggressively. Between 2019 and 2024, he fired or replaced five central bank governors who resisted his demands to cut rates. He once called interest rates "the mother and father of all evil."

Here is the body count:

| Governor | Appointed | Removed | Tenure | Why |

|---|---|---|---|---|

| Murat Çetinkaya | 2016 | Jul 2019 | 3 years | Refused to cut rates fast enough |

| Murat Uysal | Jul 2019 | Nov 2020 | 16 months | Lira hit record lows under his watch |

| Naci Ağbal | Nov 2020 | Mar 2021 | 4 months | Raised rates by 875 bps; fired overnight |

| Şahap Kavcıoğlu | Mar 2021 | Jun 2023 | 27 months | Cut rates from 19% to 8.5% as ordered |

| Hafize Gaye Erkan | Jun 2023 | Feb 2024 | 8 months | Resigned amid political pressure |

Source: Central Banking, CNBC, Wikipedia

The results were predictable to everyone except, apparently, Erdogan. Turkish inflation peaked around 85.5% in November 2022, according to official statistics (independent economists estimated the real number was closer to 170%). The lira lost more than 85% of its value against the dollar between 2018 and 2024, going from roughly 4 lira per dollar to over 35. Working-class Turks could not afford meat for months. Cooking oil tripled in price. Doctors emigrated in droves because their salaries were becoming worthless. The economic crisis touched nearly every part of Turkish society.

Turkey’s inflation and currency crisis (2018–2024) after President Erdogan fired five central bank governors. Source: CBRT, Trading Economics

Now, here is the thing: Erdogan is not stupid, and he had reasons for what he did. He believed cheaper credit would stimulate growth, boost exports through a weaker currency, and create jobs. There is actually a version of this logic that is not entirely crazy in very specific circumstances. But the evidence shows it failed catastrophically in Turkey, because the feedback loops of inflation, currency depreciation, and capital flight overwhelmed whatever short-term gains cheap credit might have produced. Erdogan was eventually forced into a humiliating U-turn, appointing an orthodox economist who jacked rates all the way to 50%. Inflation started coming back down, but the damage was already baked in.

| Metric | 2018 | 2022 (Peak Crisis) | Change |

|---|---|---|---|

| Inflation (CPI) | 16.3% | 72.3% (official) | +344% |

| USD/TRY Rate | 5.3 | 18.7 | +253% |

| Policy Rate | 24.0% | 9.0% (forced low) | -63% |

| Real Interest Rate | +7.7% | -63.3% | Deeply negative |

| Foreign Reserves | $78 billion | $40 billion (est.) | -49% |

Source: CBRT, Trading Economics, World Bank

The American Enterprise Institute recently published a piece drawing direct parallels between Turkey's trajectory and the direction the U.S. is heading. The comparison is not perfect, obviously. The U.S. has a reserve currency, deeper capital markets, and stronger institutions. But the underlying dynamic, a leader who wants rates lower than the data supports and is willing to pressure the central bank to get there, is the same.

Japan and the ECB: Independence Is Not Just an American Idea

Turkey is the extreme case, but the value of central bank independence shows up in more nuanced ways too.

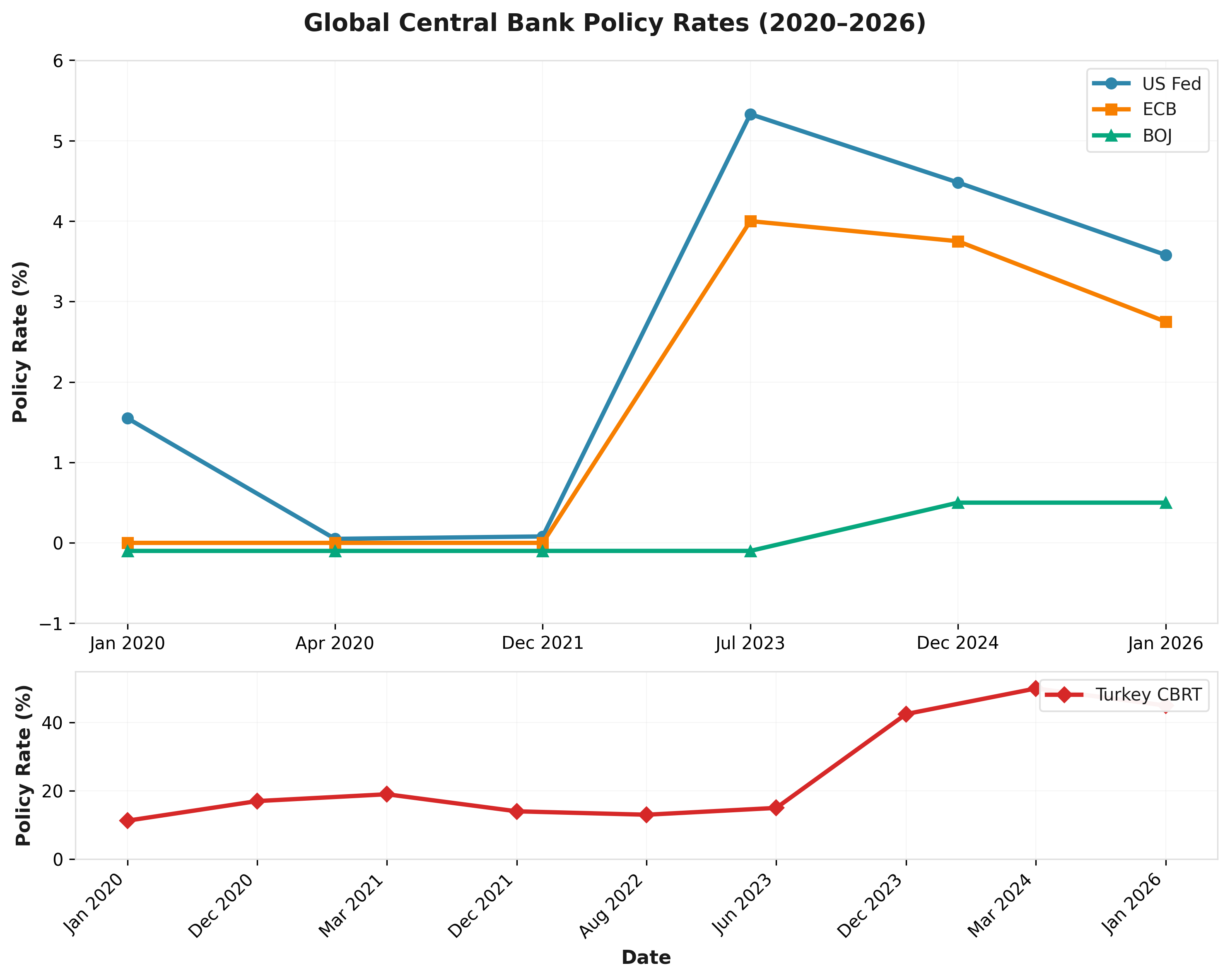

Take Japan. The Bank of Japan spent decades keeping rates at or below zero, trying to drag the country out of deflation. When inflation finally showed up after COVID and the BOJ started raising rates in March 2024 for the first time in 17 years, political figures immediately pushed back. Sanae Takaichi, who recently became Prime Minister, openly campaigned against rate hikes. When the BOJ raised rates in July 2024, the stock market dropped 18% in four days, and politicians piled on. Yet despite the political noise, the BOJ continued gradually tightening, raising its rate to 0.75% by December 2024, a 30-year high for Japan. The IMF specifically praised the BOJ for maintaining its independence and said it should keep hiking.

| BOJ Rate Decision | Date | Rate | Political Reaction |

|---|---|---|---|

| End negative rates | Mar 2024 | 0.0%–0.1% | Moderate pushback |

| First hike in 17 years | Jul 2024 | 0.25% | Nikkei crashes 18% in 4 days; politicians pile on |

| Hold | Dec 2024 | 0.25% | Government opposition blocks third hike |

| Hike | Jan 2025 | 0.50% | Takaichi (now PM) publicly opposes |

| Hold | Jan 2026 | 0.50% | BOJ holds amid snap election; IMF praises independence |

Source: Trading Economics, CNBC, Federal Reserve Bank of St. Louis

The lesson from Japan is subtler than Turkey. Nobody fired the BOJ governor. There were no criminal investigations. But there was real political pressure, and the BOJ's ability to resist it, even when the short-term market reaction was ugly, kept Japan on a credible policy path. If the BOJ had caved to political pressure and kept rates at zero, it risked letting inflation become entrenched in a country that already has massive government debt, roughly 260% of GDP, the highest in the developed world.

Then there is the European Central Bank. The ECB is an interesting counterpoint because it was designed from day one to be fiercely independent, perhaps even more so than the Fed. It only has one mandate: price stability. It does not have to worry about employment the way the Fed does. This single-minded focus has its downsides. During the European debt crisis, critics argued the ECB was too rigid and too focused on inflation while southern European countries were drowning in unemployment. There is a legitimate debate about whether the ECB's mandate is too narrow. But here is what it has not done: Europe has not experienced the kind of runaway inflation that destroys currencies and savings. The eurozone's inflation problem post-COVID was real, but it peaked at 10.6% in October 2022 and came back down to 1.7% by January 2026, because the ECB had the credibility and independence to raise rates aggressively, from 0% to 4% in just over a year, without worrying about political blowback from 20 different governments.

Global policy rate divergence since 2020. Turkey’s rates (bottom panel) dwarf all others due to political interference. Source: Trading Economics, FRED

The Independence Scorecard: The Data Does Not Lie

This is not just a collection of anecdotes. Economists have been measuring central bank independence for decades, and the correlation with inflation outcomes is one of the most robust findings in macroeconomics.

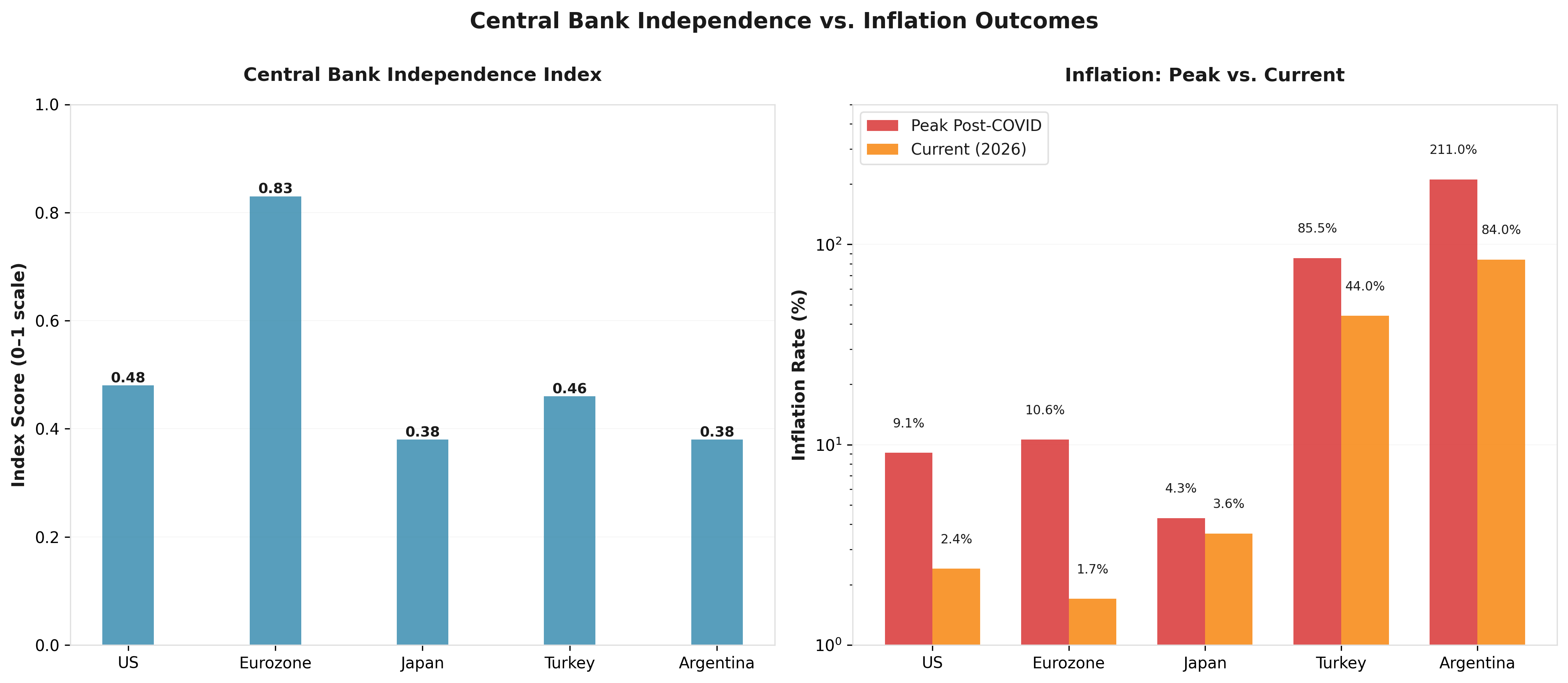

The most widely used measure is the Cukierman-Webb-Neyapti (CWN) index, which scores central bank independence on a 0-to-1 scale based on factors like governor appointment procedures, policy mandates, lending restrictions, and term lengths. A 2024 IMF working paper constructed an entirely new index, the first in three decades, and confirmed the same finding: greater central bank independence is associated with significantly lower inflation, and the benefits accumulate over time.

Countries with higher central bank independence scores consistently control inflation better. Source: IMF, Garriga CBI Dataset

| Country | CBI Index (0–1) | Peak Post-COVID Inflation | Current Inflation (Early 2026) |

|---|---|---|---|

| Eurozone | 0.83 | 10.6% | 1.7% |

| United States | 0.48 | 9.1% | 2.4% |

| Japan | 0.38 | 4.3% | 3.6% |

| Turkey | 0.46 (de jure) | 85.5% | ~44% |

| Argentina | 0.38 | 211% | ~84% |

| Venezuela | ~0.18 | ~190% | ~618% (est.) |

Source: IMF Working Paper (2024), Garriga CBI Dataset, Trading Economics, World Bank

The pattern is unmistakable. The Eurozone, which has the highest formal independence score in the world, brought inflation back to target fastest. Turkey, which has a reasonable score on paper but effectively zero independence in practice because Erdogan fires anyone who disagrees with him, experienced inflation 8x worse than the U.S. at its peak. Argentina and Venezuela, where central banks have been treated as government piggy banks for decades, are in a league of their own.

A 2024 CEPR study found that improvements in central bank independence yield long-lasting benefits and that central bank independence reduces inflation persistence, meaning the effects of price shocks fade faster in countries where central banks are free to respond without political interference.

Does the Fed Deserve Criticism? Absolutely.

I want to be clear about something: arguing for Fed independence is not the same as arguing the Fed is perfect. It is not. And pretending otherwise weakens the case for independence, not strengthens it.

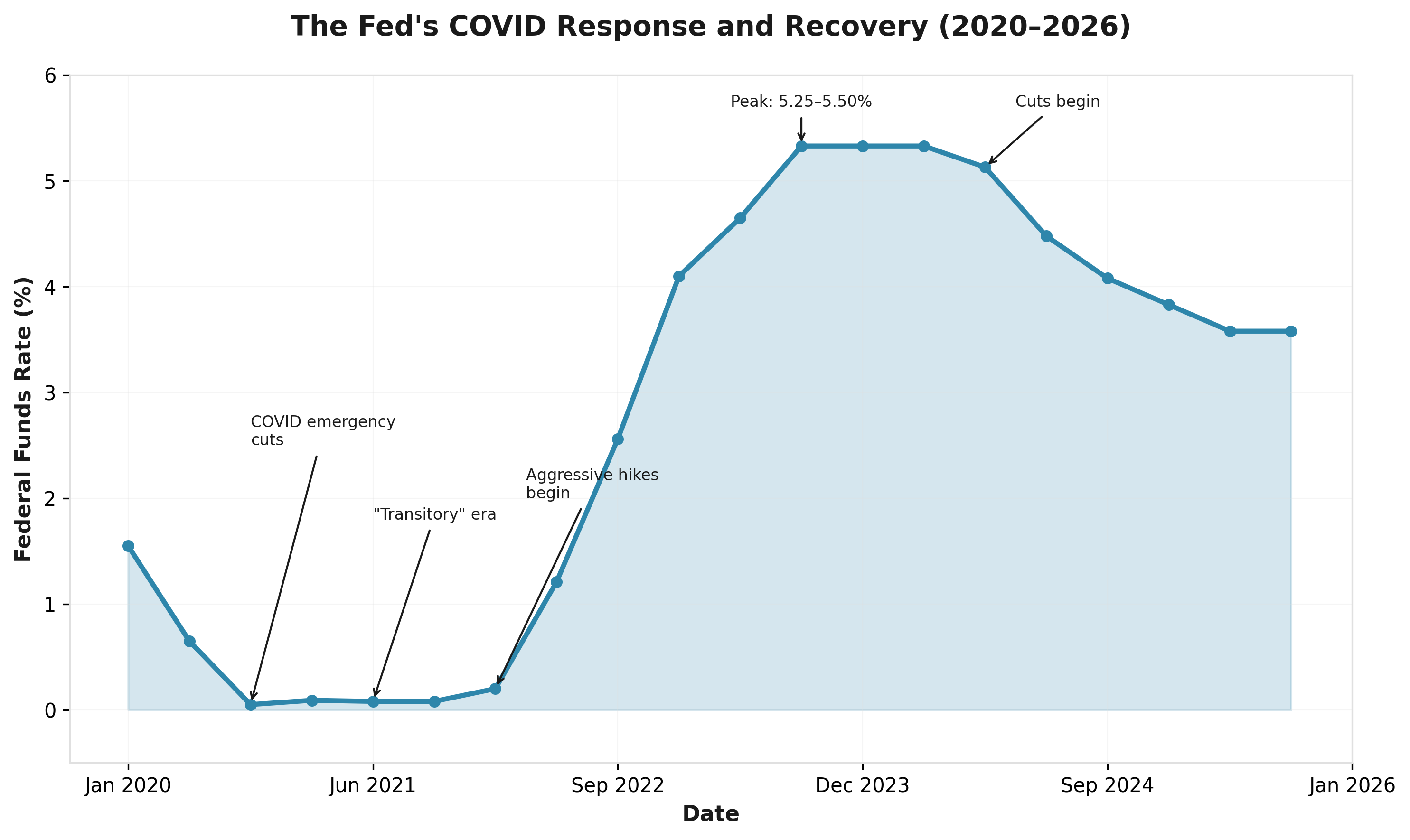

The Fed was too slow to raise rates after COVID. Full stop. When inflation started climbing in 2021, Chair Powell and other officials kept calling it "transitory." They held rates near zero well into 2022, even as prices were clearly running hot. By the time they started hiking aggressively, inflation had hit 9.1% in June 2022, the highest in 40 years. The Fed did not raise rates above zero until March 2022, a full year after inflation first exceeded 2%.

The Fed’s COVID-era rate cycle: emergency cuts to near-zero, the “transitory” delay, aggressive hikes, and the 2024–25 easing. Source: FRED

| Date | Fed Action | Inflation (CPI YoY) | Fed Funds Rate |

|---|---|---|---|

| Mar 2020 | Emergency cut to near-zero | 1.5% | 0.05% |

| Mar 2021 | Still holding at zero | 2.6% | 0.07% |

| Jun 2021 | Still holding ("transitory") | 5.4% | 0.08% |

| Dec 2021 | Still holding | 7.0% | 0.08% |

| Mar 2022 | First hike (+25 bps) | 8.5% | 0.20% |

| Jun 2022 | Aggressive hikes begin (+75 bps) | 9.1% | 1.21% |

| Jul 2023 | Final hike to peak | 3.2% | 5.33% |

| Sep 2024 | First cut (-50 bps) | 2.4% | 5.13% |

| Dec 2025 | Three more cuts in 2025 | 2.7% | 3.58% |

Source: Bureau of Labor Statistics, FRED, CBS News, PBS

Why did this happen? Part of it is the data lag problem. The Fed relies on economic data that is inherently backward-looking. Employment numbers, inflation readings, GDP figures, all of it tells you what already happened, not what is about to happen. When the economy changes quickly, as it did during COVID, the data takes months to catch up. The Fed was essentially driving by looking in the rearview mirror.

This is a real structural weakness, and it is fair to criticize the Fed for it. Kevin Warsh, the man Trump nominated today, has been vocal about this exact point. He has argued the Fed's forecasting methodology fails at identifying turning points and that it should take a more forward-looking approach. He is not wrong about the diagnosis.

If the Fed, staffed with hundreds of PhD economists with access to the most sophisticated economic data in the world, can still make mistakes because of data lags and model limitations, imagine how much worse those mistakes would be if the person making the call was a politician whose primary concern was the next election. The Fed being imperfect is an argument for reforming the Fed. It is not an argument for handing monetary policy to the president.

And for what it is worth, the Fed under Powell also showed why independence matters on the other side of the coin. In 2024, with a presidential election approaching, the Fed started cutting rates, beginning with a 50-basis-point cut in September. It then cut again in November and December, bringing the total to 100 basis points of easing in four months. Trump and his allies accused Powell of playing politics, trying to boost the economy to help Biden. But the data actually supported the cuts. The labor market was softening, inflation had come down from 9.1% to around 2.4%, and the Fed was trying to engineer a soft landing. Powell cut rates even though he knew it would invite accusations of political motivation. An independent Fed can absorb that criticism. A Fed controlled by the president could not make that kind of decision without it being seen as purely political.

The Trump-Powell Saga: How We Got Here

The irony of the Trump-Powell feud is that Trump is the one who picked Powell in the first place, back in 2017. By his own account, he later regretted it, blaming former Treasury Secretary Steve Mnuchin for the recommendation.

The tension has always been about one thing: Trump wants rates lower than Powell is willing to go. During his first term, Trump called Powell a "major loser" and a "fool" and once suggested the Fed Chair was a bigger threat to America than the president of China. Most people expected the rhetoric to soften in the second term. It did not.

In 2025, the Fed cut rates three times in the back half of the year to support the labor market, bringing the target range down to 3.50%–3.75%. But Powell said future cuts would be cautious because inflation was still above the 2% target. Trump wanted more. He wanted rates at "rock-bottom levels." He also tried to fire Fed Governor Lisa Cook over fraud allegations, marking the first time a president has attempted to remove a sitting Fed governor.

The renovation saga became the pressure point. The Fed's headquarters renovation grew from $1.9 billion to $2.5 billion. Trump's allies claimed it included luxury features like beehives and rooftop gardens. Powell denied all of it under oath. In July 2025, Trump toured the project with Powell and claimed the cost was $3.1 billion. Powell corrected him on the spot, pointing out Trump had added a separate building that was finished five years earlier. Seven awkward seconds of silence followed.

Then, earlier this month, the DOJ launched a criminal probe into Powell regarding his Congressional testimony about the renovation. Powell responded with a video statement that was, by Fed Chair standards, absolutely explosive. He accused the administration of using federal prosecutors to pressure the Fed on interest rate decisions, calling it a pretext and warning that the real issue was whether the Fed could continue setting rates based on economic evidence or whether it would be directed by political intimidation.

Trump, to his credit, has reasons for wanting lower rates that are not purely self-serving. Lower rates do stimulate growth. They make housing more affordable (the average 30-year mortgage rate was hovering around 6.5% in early 2026, compared to the 3% range during COVID). They reduce the government's own borrowing costs, which matters when the national debt is north of $36 trillion and annual interest payments have surpassed $1 trillion. These are not frivolous points. The disagreement is not about whether lower rates would be nice. The disagreement is about who gets to make the call and on what timeline.

Enter Kevin Warsh

Which brings us to this morning's news. Trump nominated Kevin Warsh to succeed Powell, and the pick is more interesting than you might expect.

Warsh is 55, a former Fed Governor who served from 2006 to 2011 and was the youngest person ever confirmed to the Board at age 35. He was part of Ben Bernanke's inner circle during the 2008 financial crisis, serving as the Fed's main point of contact with Wall Street. Bernanke himself described Warsh and Don Kohn as his "most frequent companions" during the crisis. Warsh helped engineer emergency responses, warned colleagues early that the financial system was undercapitalized, and was tasked with devising financial reforms after the crisis.

His resume is stacked: Stanford undergrad, Harvard Law, Morgan Stanley M&A, White House National Economic Council under George W. Bush. Since leaving the Fed, he has been at Stanford's Hoover Institution and worked as a partner at Stanley Druckenmiller's family office. His father-in-law is Ronald Lauder, a billionaire who has been close with Trump since their days at Wharton together, which certainly did not hurt his candidacy.

Here is what is interesting about Warsh: he used to be a well-known inflation hawk. During his time on the Board, he was skeptical of QE2 and told Bernanke directly that he would not be leading the committee in that direction if he were chair. He resigned in 2011 partly out of concern the Fed was pumping too much money into the system. That is not the profile of someone who will blindly follow Trump's demands for rock-bottom rates.

But Warsh has shifted. In a Wall Street Journal op-ed last year, he argued that AI-driven productivity gains could be a major disinflationary force, creating room for lower rates without risking inflation. He has also said he thinks the Fed should abandon what he calls "the dogma that inflation is caused when the economy grows too much and workers get paid too much." When Trump asked him directly about rates in December, Warsh reportedly told him he thinks borrowing costs should be lower. Some commentators have called him a "chameleon." Others say his views have evolved for legitimate reasons.

| Kevin Warsh | Then (2006–2011) | Now (2025–2026) |

|---|---|---|

| Inflation stance | Hawk; skeptical of QE2 | More flexible; sees AI as disinflationary |

| Rate preference | Higher for longer | Lower than current levels |

| Fed independence | Strongly defended | Says it depends on "public confidence" |

| Key influence | Bernanke inner circle | Druckenmiller family office, Hoover Institution |

| View on forecasting | N/A | Fed models fail at turning points; needs reform |

Warsh has also publicly said that the Fed's effectiveness depends on public confidence that its decisions are driven by economics, not politics. Whether he actually holds that line when Trump inevitably calls for deeper cuts is the open question.

What Happens Next: The Senate Confirmation

Warsh's path to the chair is not guaranteed, and the Senate process could get complicated.

Under U.S. law, the nomination first goes to the Senate Banking Committee, which holds hearings, reviews financial disclosures, and conducts a public confirmation hearing. The committee then votes on whether to send the nomination to the full Senate for a final confirmation vote, which requires a simple majority. The typical process takes somewhere between four and ten weeks, though political dynamics can stretch that significantly.

Here is where it gets tricky. The Senate Banking Committee has a 13-11 Republican majority. Under normal circumstances, that would be plenty to push Warsh through. But Republican Senator Thom Tillis of North Carolina has already announced, just hours after the nomination, that he will oppose the confirmation of any Fed nominee until the DOJ investigation into Powell is resolved. His exact words: "Protecting the independence of the Federal Reserve from political interference or legal intimidation is non-negotiable."

That matters because of the math. If Tillis votes no alongside all 11 Democrats on the committee, the vote would deadlock at 12-12, and the nomination would not advance to the full Senate floor. One Republican defection is all it takes to stall the entire process.

| Scenario | Committee Vote | Outcome |

|---|---|---|

| Party-line vote (all Rs yes) | 13-11 | Advances to full Senate |

| Tillis defects, all Ds vote no | 12-12 | Deadlocked; does not advance |

| Two GOP defections | 11-13 | Rejected in committee |

| Confirmation drags past May 2026 | N/A | VP Philip Jefferson becomes acting Chair |

Banking Committee Chairman Tim Scott has said he wants a "thoughtful, timely confirmation process," but there is only so much he can do if Tillis holds firm. And Tillis, who is not running for reelection, has less political incentive to fold than most.

If the confirmation drags past May, when Powell's term as chair expires, Vice Chair Philip Jefferson would step in as acting chair. Powell himself could remain on the Board of Governors (his board term does not expire until 2028), but it is unclear whether he would choose to stay.

The irony is thick: the very investigation that Trump's administration launched against Powell could be the thing that delays his own nominee from taking the job. Warsh is widely seen as qualified for the role. Even Tillis has praised him. But Tillis is making a principled stand that the DOJ probe needs to be resolved first, and that stand has real procedural teeth.

If Warsh does make it through, most analysts expect one or two rate cuts in 2026, with his first FOMC meeting likely in June. The bigger questions will be about the Fed's balance sheet and whether Warsh follows through on his stated desire for "regime change" at the central bank. His confirmation hearing will be one of the most closely watched events in monetary policy this year.

Why This Should Matter to You

If you are in your twenties right now, this stuff is going to shape your financial life more than almost any other policy question. Interest rates flow through everything: your student loans, your future mortgage, the job market you are entering, the returns on your retirement savings. A Fed that makes decisions based on data, even if it sometimes gets those decisions wrong, produces a fundamentally more stable economy than one that takes marching orders from the Oval Office.

The track record is not ambiguous. Countries with independent central banks have lower inflation, more stable currencies, and deeper capital markets. Countries where politicians run monetary policy get Turkey. They get Argentina. They get Venezuela. The American economy's long-term track record of growth is not an accident. It was built on institutions that work, and the Fed's independence is one of the most important.

Consider the numbers one more time: the U.S. brought inflation from 9.1% back down to 2.4% in about two and a half years, painful but controlled. Turkey, where the president ran the show, saw inflation explode to 85% and is still at 44% years later. Argentina, where the central bank has been used to finance government spending for decades, hit 211% inflation in 2023. Venezuela, the most extreme case, is running above 600%. The pattern holds in every direction you look.

The Bottom Line

The Trump-Powell fight has been messy, personal, and at times kind of absurd. A feud about a building renovation turned into a criminal investigation turned into a constitutional crisis in slow motion. And now, today, we have a new nominee who walks into one of the most politically charged transitions in the Fed's history.

Kevin Warsh has the background to handle it. The Senate confirmation process will test whether he can credibly commit to independence. The institutions are being stressed, but they have survived worse. The Fed made it through the 1970s. It will probably make it through this too.

The boring stuff, the institutional guardrails, the 14-year terms, the "for cause" removal protections, all of that exists for a reason. And as long as enough people understand why it matters, it is going to hold.

Sources: , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,