The New American Playbook

I woke up on January 3rd to a notification that American special forces had captured Nicolás Maduro in a nighttime raid on Caracas. Like most people, my first reaction was shock. My second reaction, almost immediately after, was to check oil futures. That instinct tells you everything about what this moment really is: the collision of hard power politics with energy economics on a scale we have not seen since the Iraq War.

Nearly two months later, Venezuela is being governed by a former Maduro loyalist, American oil companies are circling 303 billion barrels of proven reserves, and the “Donroe Doctrine” has entered the foreign policy lexicon. But the real story here is not just about one country. Venezuela was a proof of concept. And the next chapter, likely involving Iran, could reshape global energy markets in ways that make the Maduro raid look like a footnote.

What Actually Happened

On January 3, 2026, the United States executed Operation Absolute Resolve. Delta Force operators, supported by over 150 aircraft and backed by months of CIA intelligence gathering, breached Maduro’s compound in Caracas in the early morning hours. Maduro and his wife, Cilia Flores, were taken into custody, transported to the USS Iwo Jima, and flown to New York City. By January 5, Maduro was standing in a Manhattan federal courtroom, pleading not guilty to narco-terrorism and drug trafficking charges that had been filed years earlier.

The operation itself was tactically precise. American fighters neutralized Venezuelan air defenses (purchased from Russia, but ultimately useless against the world’s most advanced military), and the entire extraction took place with minimal resistance. Cuba later reported 32 of its personnel were killed during the operation, revealing how deeply intertwined foreign actors had become with the Maduro regime.

Within days, Vice President Delcy Rodríguez was sworn in as interim president. Trump, rather than backing opposition leader María Corina Machado (the widely recognized winner of the 2024 election and 2025 Nobel Peace Prize laureate), signaled that his administration would work with Rodríguez. That decision confused many observers, but it made a certain kind of pragmatic sense: Rodríguez controls the military, she holds the bureaucratic levers, and she showed a willingness to cooperate with Washington almost immediately.

The Donroe Doctrine: What It Is and Why It Matters

To understand why this happened, you have to understand the framework the Trump administration built before a single helicopter left the ground.

In November 2025, the administration released its National Security Strategy, which included an explicit section titled “The Trump Corollary to the Monroe Doctrine.” The language was blunt: the United States would “reassert and enforce the Monroe Doctrine to restore American preeminence in the Western Hemisphere” and “deny non-Hemispheric competitors the ability to position forces or other threatening capabilities, or to own or control strategically vital assets, in our Hemisphere.”

The original Monroe Doctrine, articulated by President James Monroe in 1823, warned European powers against colonizing or interfering in the Americas. It effectively drew a line around the Western Hemisphere and said: this is our neighborhood. Various presidents have invoked it since, from Teddy Roosevelt’s “Big Stick” approach to Reagan’s Cold War interventions in Central America.

Trump’s version, quickly dubbed the “Donroe Doctrine” (a portmanteau of Donald and Monroe that the New York Post coined and Trump himself later adopted), goes further. It is not just about keeping foreign powers out. It is about actively reasserting American economic and military dominance across the hemisphere, with an explicit focus on countering Chinese influence.

China’s footprint in Venezuela by the numbers: $67 billion invested since 2007 (primarily energy sector), $60 billion in cumulative state loans, ~90% of Venezuelan oil exports flowing to China by late 2025, and $6 billion in bilateral trade in the first 11 months of 2025. China also delivered an average of 1.38 million barrels per day of Iranian crude and condensate in 2025, making Beijing the indispensable customer for both countries the U.S. targeted.

By late 2025, China had become the leading trade partner of nearly every country in South America. China-Latin America trade volume hit a record $518 billion in 2024, and at a Beijing summit in May 2025, Xi Jinping announced a $9 billion investment credit line for the region. The Donroe Doctrine was, at its core, a declaration that this arrangement was over.

Venezuela became the doctrine’s first real test. When Trump held his Mar-a-Lago press conference after Maduro’s capture, he did not mince words: “American dominance in the Western Hemisphere will never be questioned again.” Whether you view this as justified realpolitik or neo-imperialism depends on your priors. But from an economic standpoint, the doctrine has teeth, and the Venezuela operation proved it.

This Has Happened Before

The Maduro capture did not emerge from a vacuum. American presidents have a long track record of using military force to remove leaders in the Western Hemisphere, and each historical parallel reveals something about the Venezuela playbook.

| Operation | Year | Target | Justification | Oil Reserves (bn bbl) | Outcome |

|---|---|---|---|---|---|

| Urgent Fury | 1983 | Grenada | Protect U.S. citizens, counter Cuba | 0 | Stable democracy |

| Just Cause | 1989 | Panama (Noriega) | Drug trafficking charges | 0 | Stable democracy |

| Iraqi Freedom | 2003 | Iraq (Saddam) | WMDs / security threat | 145 | Years of insurgency |

| Unified Protector | 2011 | Libya (Gaddafi) | Humanitarian / R2P | 48 | Failed state |

| Absolute Resolve | 2026 | Venezuela (Maduro) | Drug trafficking / Monroe Doctrine | 303 | TBD |

The closest analogue is Panama in 1989. President George H.W. Bush ordered Operation Just Cause to capture Manuel Noriega, who, like Maduro, had been indicted on drug trafficking charges in the United States. The operation was fast, decisive, and framed around law enforcement rather than regime change. Noriega was extracted, put on trial in Miami, and convicted. The parallels are almost eerie: a Latin American strongman, drug charges filed in American courts, a swift military operation, and a new government installed within days.

Grenada in 1983 offers another relevant comparison, though a more limited one. Reagan’s intervention was a quick Caribbean strike justified on the grounds of protecting American citizens and countering Cuban influence. It was over in days, the geopolitical stakes were comparatively low, and it served primarily as a signal of American willingness to use force in its backyard. Venezuela was a much larger and more complex operation, but the signaling function was identical.

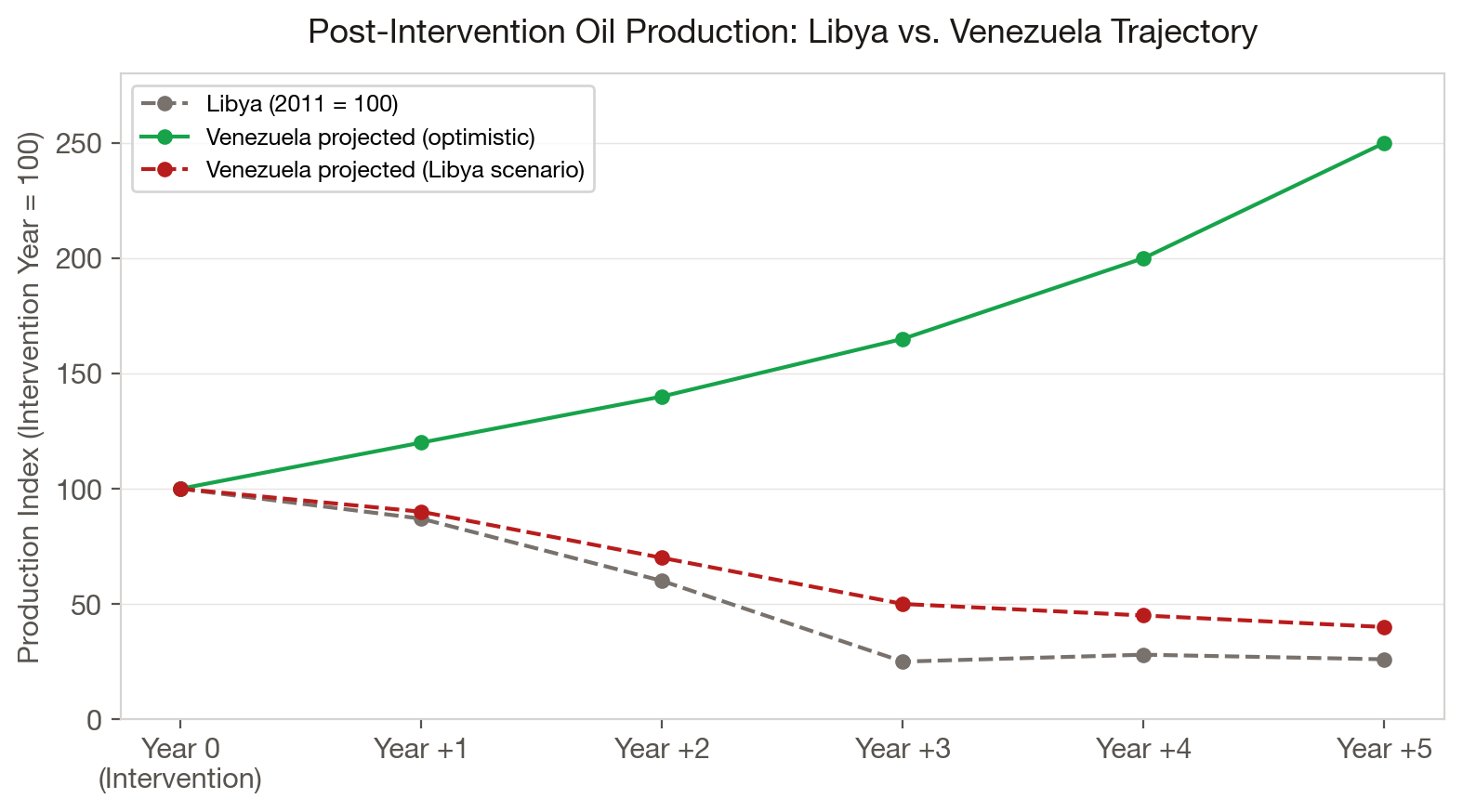

Libya in 2011 is the comparison that should worry people the most. The NATO-backed removal of Muammar Gaddafi succeeded tactically but produced years of chaos. Libya descended into civil war, became a failed state, and its oil production collapsed. Several analysts have already drawn the parallel, noting that Venezuela could follow a similar trajectory if political instability persists after Maduro’s removal.

Libya’s post-intervention oil production collapse is the cautionary tale for Venezuela. Source: EIA, Rystad Energy, CEIC Data

And then there is Iraq in 2003, the elephant in the room. The Bush administration’s invasion to remove Saddam Hussein was justified on security grounds, but the oil subtext was always present. Iraq sits on the world’s fifth-largest proven oil reserves at 145 billion barrels; Venezuela sits on the first at 303 billion. Both operations resulted in American officials openly discussing plans for Western oil companies to enter the country and rebuild energy infrastructure. The difference, at least so far, is that the Venezuela operation was significantly more contained: a targeted capture rather than a full-scale invasion, with no plans for a prolonged ground occupation.

Each of these precedents teaches the same lesson: tactical success is the easy part. The hard part is what comes after.

The Oil Equation

This is where the economics get interesting, and where I think most of the mainstream coverage has been too surface-level.

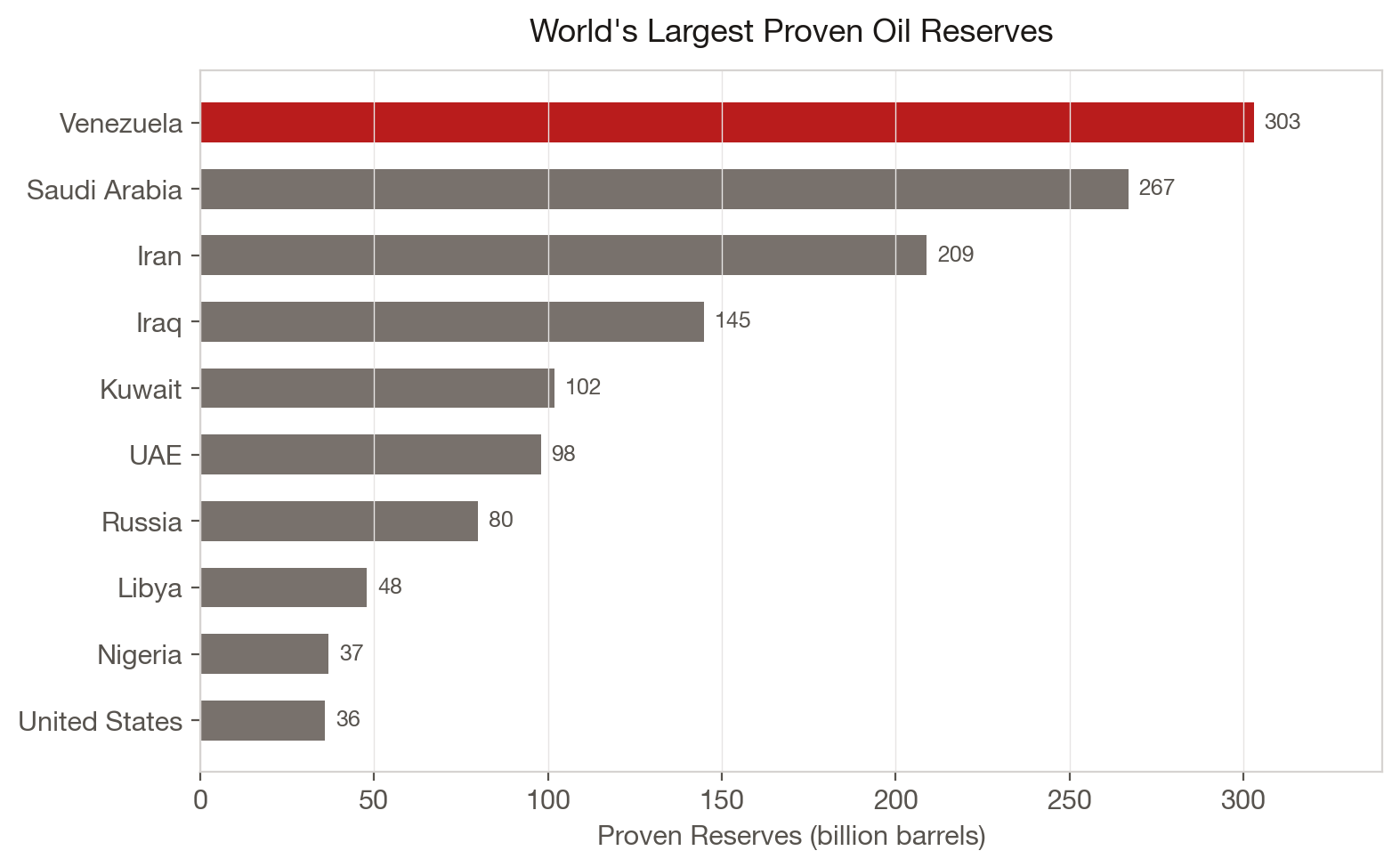

Venezuela holds 17% of global proven oil reserves, more than any other country. Source: OPEC, Worldometer

Venezuela holds an estimated 303 billion barrels of proven crude oil reserves, roughly 17% of the 1.77 trillion barrel global total. On paper, that makes it the most oil-rich country on the planet, ahead of Saudi Arabia (267 billion), Iran (209 billion), and Iraq (145 billion). In practice, it has been one of the most underperforming.

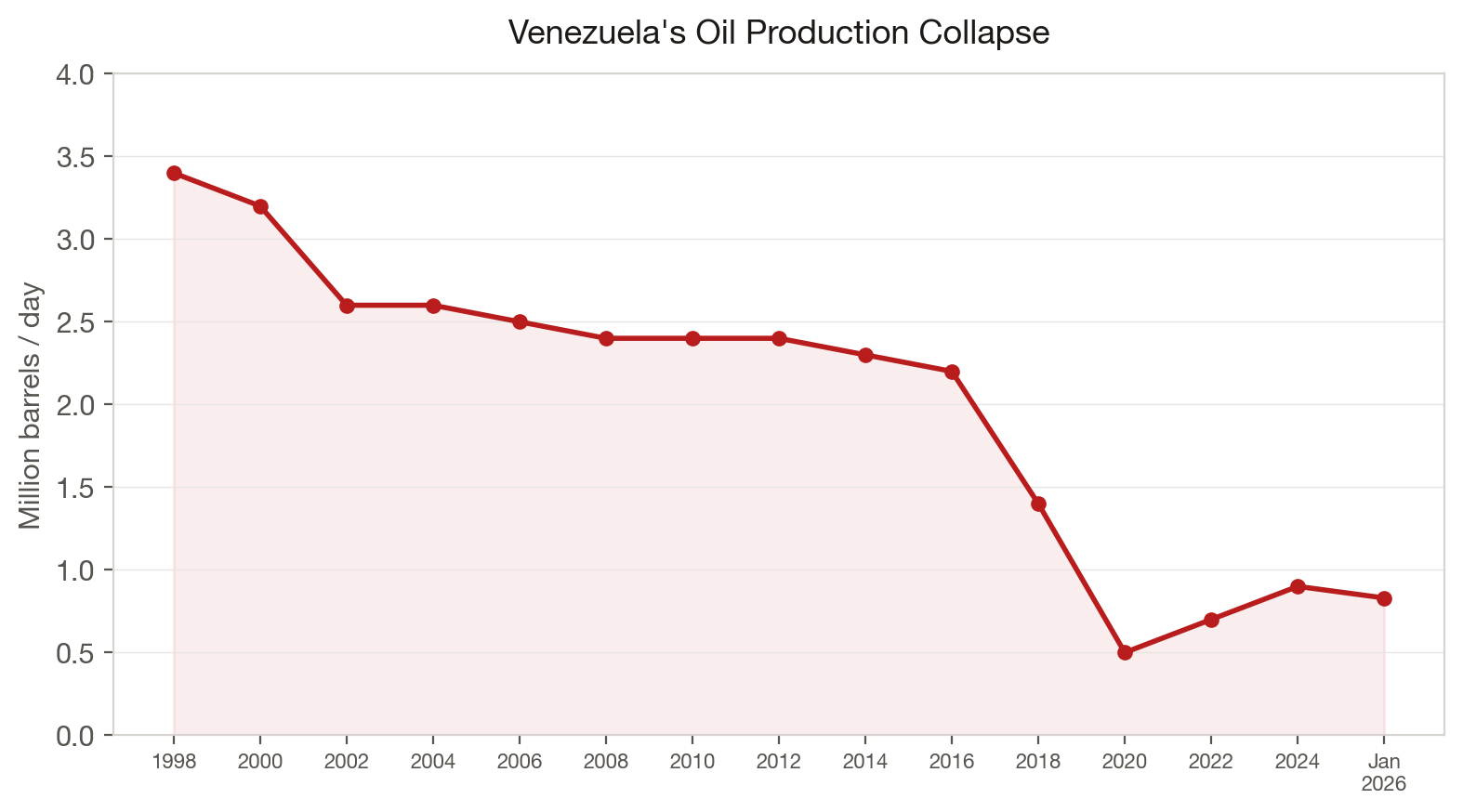

A two-decade collapse: from 3.4 million barrels per day to under 1 million. Source: EIA, CEIC Data, OPEC

Under Maduro, production collapsed from a peak of about 3.4 million barrels per day in the late 1990s to approximately 800,000–900,000 barrels per day by late 2025. The nadir came in mid-2020, when output cratered to as low as 337,000 barrels per day, a 90% decline from the peak. Years of mismanagement, corruption, a brain drain of technical expertise, and crushing U.S. sanctions hollowed out the state oil company PDVSA. The country’s pipelines have not been updated in 50 years.

| Year | Production (million bpd) | Change from Peak | Key Event |

|---|---|---|---|

| 1998 | 3.4 | — | Peak output; Chávez elected |

| 2002 | 2.6 | -24% | PDVSA strike / mass firings |

| 2007 | 2.5 | -26% | ExxonMobil & ConocoPhillips nationalized |

| 2010 | 2.4 | -29% | Chronic underinvestment deepens |

| 2015 | 2.3 | -32% | Oil price crash; economic crisis begins |

| 2019 | 0.9 | -74% | U.S. sanctions imposed |

| 2020 | 0.5 | -85% | COVID + sanctions nadir (337k bpd low) |

| 2024 | 0.9 | -74% | Partial recovery under Chevron license |

| Jan 2026 | 0.83 | -76% | Post-capture disruption |

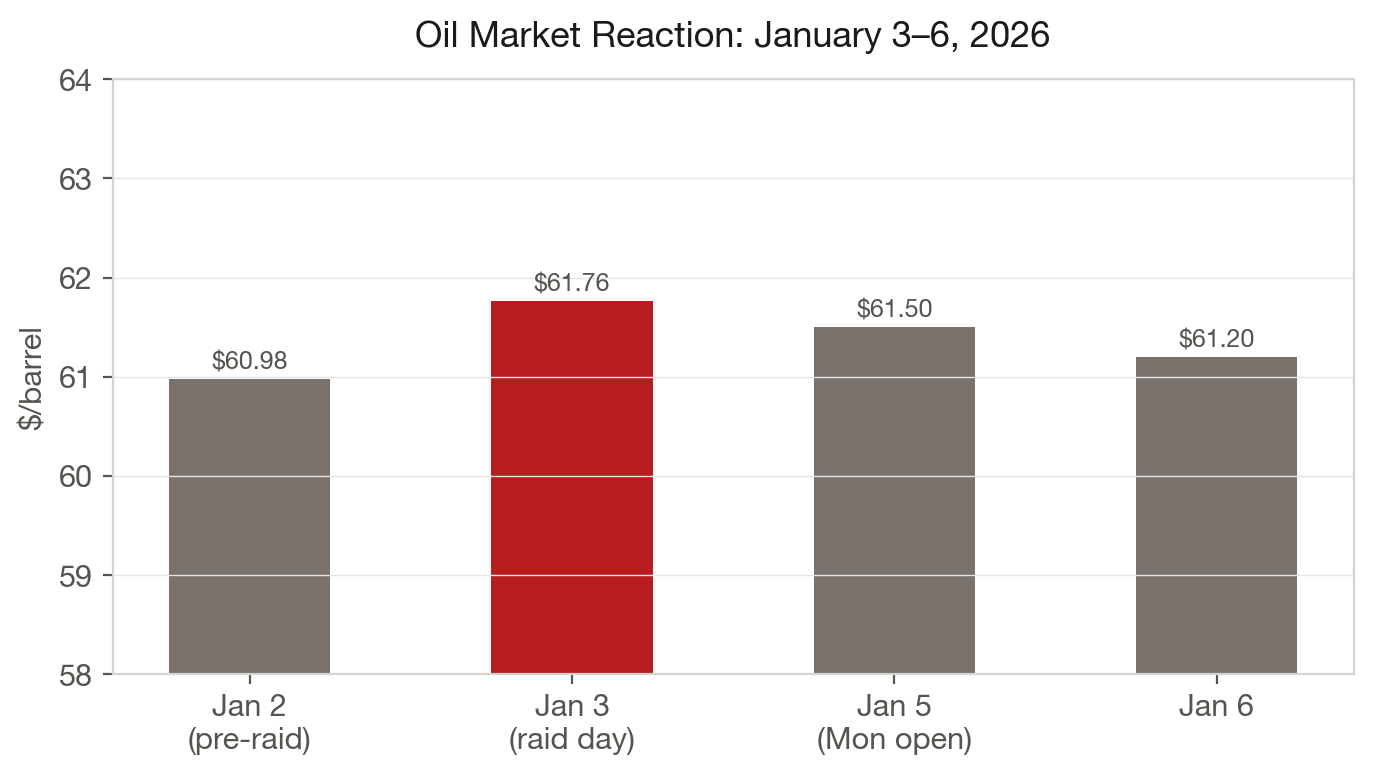

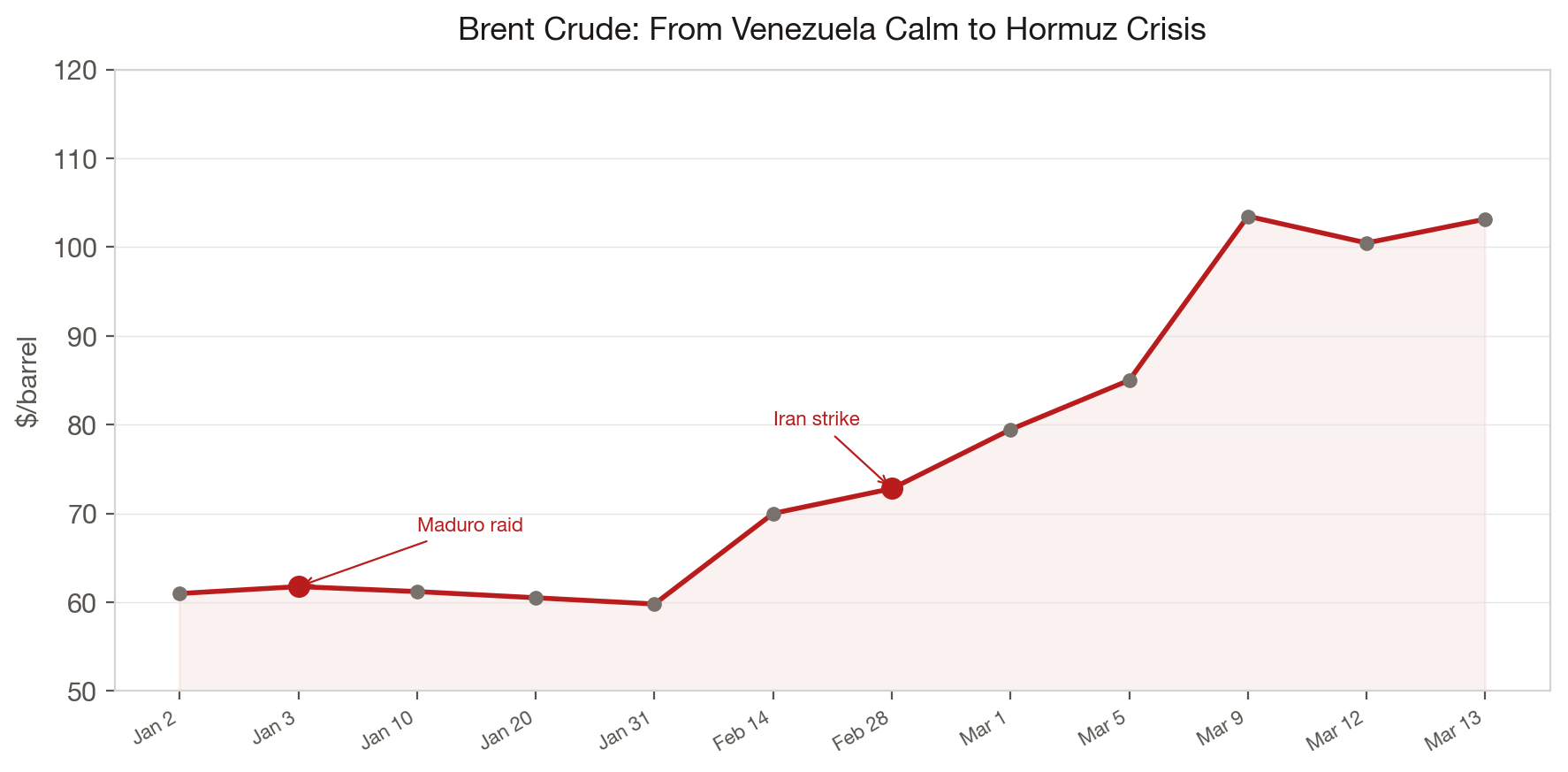

So when oil markets opened after the capture, the reaction was notably muted. Brent crude, assessed at $60.98/barrel the day before the raid, ticked up about 1.7% to settle at $61.76. The consensus among energy analysts was clear: Venezuela accounts for less than 1% of global crude production. In a world already dealing with an oil glut (the IEA projected a global supply surplus of nearly 4 million barrels per day for 2026), losing some Venezuelan barrels was a rounding error.

Brent crude barely moved after the Maduro capture. Source: S&P Global Platts, CNBC

But the medium-to-long-term story is different, and this is the part that matters for anyone paying attention to energy markets. Venezuelan crude is heavy, sour oil. It is the kind of crude that U.S. Gulf Coast refineries were specifically built to process. About 70% of American crude imports are heavy oil, and much of that currently comes from Canada. If Venezuelan production can be rehabilitated (and that is a big “if”), it would diversify heavy crude supply for American refiners, reduce dependence on Canadian imports, and give Washington significant leverage over a critical input to diesel, asphalt, and industrial fuel production.

| Company | Stock Move (Jan 5) | Venezuela Status | Estimated Claim / Position |

|---|---|---|---|

| Chevron (CVX) | +6.4% | Active (OFAC license) | ~23% of Venezuela output via JVs |

| ExxonMobil (XOM) | +3.0% | Assets nationalized 2007 | Arbitration award pending |

| ConocoPhillips (COP) | +5.5% | Assets nationalized 2007 | $8.5B ICSID award (2019) |

| SLB (Schlumberger) | +4.2% | Services provider | Major infrastructure rebuild contracts expected |

| Halliburton (HAL) | +3.8% | Services provider | Well services & drilling expected |

Source: CNBC, S&P Global Platts

Energy Secretary Chris Wright announced that Washington intends to oversee the sale of Venezuelan oil “indefinitely.” Trump himself said American oil companies would “go in, spend billions of dollars, fix the badly broken infrastructure.” Estimates from RBC Capital Markets suggest Venezuelan production could grow by several hundred thousand barrels per day over the next 12 months if sanctions are fully lifted and the security environment stabilizes. More optimistic projections put output at 1.1 to 1.2 million barrels per day by end of 2026.

The rehabilitation price tag: Rystad Energy estimates $53 billion in upstream and infrastructure investment over 15 years just to hold production flat at 1.1 million bpd. To reach 3 million bpd by 2040, the total capex required is an estimated $183 billion, with at least $30–35 billion in international capital needed in the next 2–3 years. More than $65 billion is required solely to repair, upgrade, and rebuild Venezuela’s aging pipelines and facilities.

The catch is cost. Industry executives estimate it will take around $8–9 billion annually to meaningfully turn production around, and the political situation needs to be stable enough for companies to commit that kind of capital. That brings us to the new leadership.

What Rodríguez Is Actually Doing

Delcy Rodríguez has moved fast. In her first month as interim president, she signed a reform to the Organic Law on Hydrocarbons that ended PDVSA’s monopoly over oil production and sales, opening the door for private domestic and foreign companies to operate directly. She announced that Venezuela received $300 million from the first tranche of U.S.-facilitated crude oil sales, part of a $500 million agreement. She signed an amnesty law covering political offenses dating back to 1999 and ordered the shutdown of El Helicoide, the notorious intelligence prison in Caracas where torture had been extensively documented.

These moves are significant. They signal that Rodríguez understands the price of continued American cooperation: tangible reforms on oil access, political prisoners, and governance. Former U.S. Ambassador James Story characterized her strategy as doing “just enough to make it look as if they’re complying” while waiting for Washington’s attention to shift. That is probably accurate. Rodríguez is a lifelong Chavista who spent years enabling the Maduro regime. Her reforms are transactional, not ideological.

But transactions can be enough if the incentives align. Right now, Rodríguez needs American military restraint and economic engagement. Washington needs oil access and a cooperative government in Caracas. As long as that mutual dependency holds, the reforms will continue. Whether they lead to genuine democratic transition or just a rebranded version of authoritarian governance (what some analysts are calling “Madurismo without Maduro”) is the open question.

Iran: The Next Domino

Here is where I want to shift from analysis to prediction, because I believe the Venezuela operation was not an isolated event. It was phase one.

Since Operation Midnight Hammer in June 2025, when U.S. B-2 bombers struck three Iranian nuclear facilities at Fordow, Natanz, and Isfahan, the relationship between Washington and Tehran has been on a knife’s edge. The strikes inflicted severe damage to Iran’s enrichment capabilities, but they did not eliminate the program entirely. IAEA officials have said Iran could reconstitute centrifuge cascades within months.

Negotiations have gone nowhere. Indirect talks in Oman in early February produced what Iranian Foreign Minister Araghchi called a “good start,” but the fundamental gap remains: Washington demands zero enrichment, Tehran insists on its right to a civilian nuclear program. Trump said on February 27 that he was “not happy” with the progress.

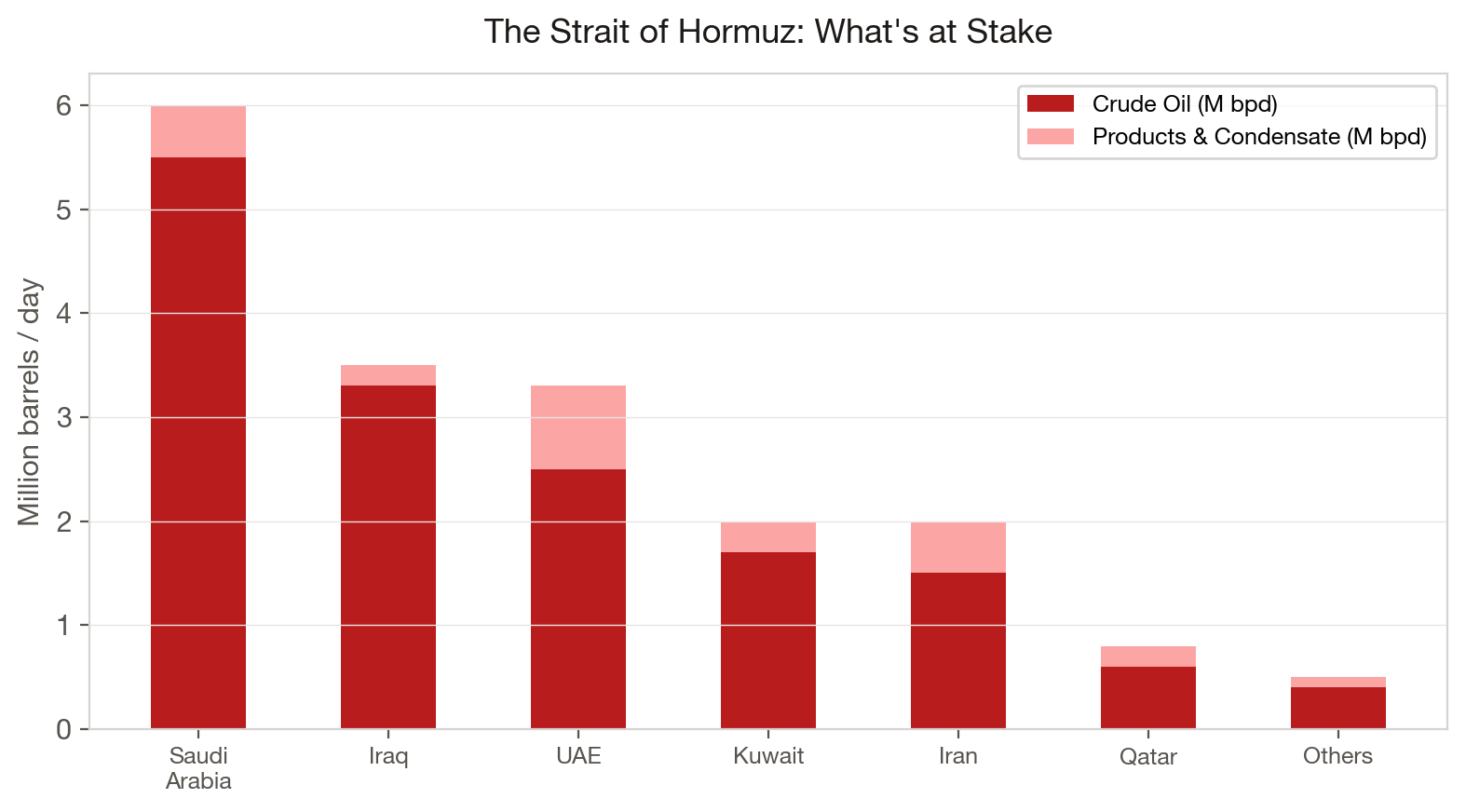

| Metric | Venezuela | Iran | Iran + Hormuz |

|---|---|---|---|

| Daily production | ~830K bpd | ~3.2M bpd | — |

| Share of global supply | <1% | ~3.2% | ~20% |

| Daily flow at risk | ~500K bpd exports | ~2M bpd exports | 20M bpd through Hormuz |

| Primary customer | China (~90%) | China (~1.4M bpd) | Asia (China, India, Japan, Korea) |

| Proven reserves | 303B bbl | 209B bbl | — |

| Brent price impact (Jan 3) | +1.7% | — | — |

| Projected price impact (full disruption) | ~$1/bbl | ~$4/bbl | $12–15/bbl (GS model) |

Source: EIA, IEA, Goldman Sachs Research

Meanwhile, the military posture tells a different story than the diplomatic one. Trump posted on Truth Social on January 28 that a “massive armada is heading to Iran.” War-risk insurance premiums for the Strait of Hormuz have already increased significantly, rising from 0.125% to between 0.2% and 0.4% of ship value per transit. For a very large crude carrier valued at around $100 million, that is an increase of roughly a quarter of a million dollars per trip. Reports indicate Iran has been rapidly accelerating its oil exports over the past two weeks, a classic signal that a government is trying to front-load revenue before a disruption.

If the United States strikes Iran again, the oil market impact will be fundamentally different from Venezuela. Iran produces around 3.2 million barrels per day of crude and exports roughly 2 million bpd. But the real risk is not Iranian production itself. It is the Strait of Hormuz.

Nearly 20 million barrels per day of oil flows through that strait, representing about 20% of global petroleum consumption and 34% of all seaborne crude trade. Saudi Arabia alone accounts for 5.5 million bpd through Hormuz (38% of total strait flows). It is also the transit route for roughly 20% of global LNG trade. If Iran retaliates by disrupting Hormuz traffic, either through direct attacks on tankers, mining, or simply threatening enough violence that commercial shipping insurers pull coverage, the price impact would be enormous.

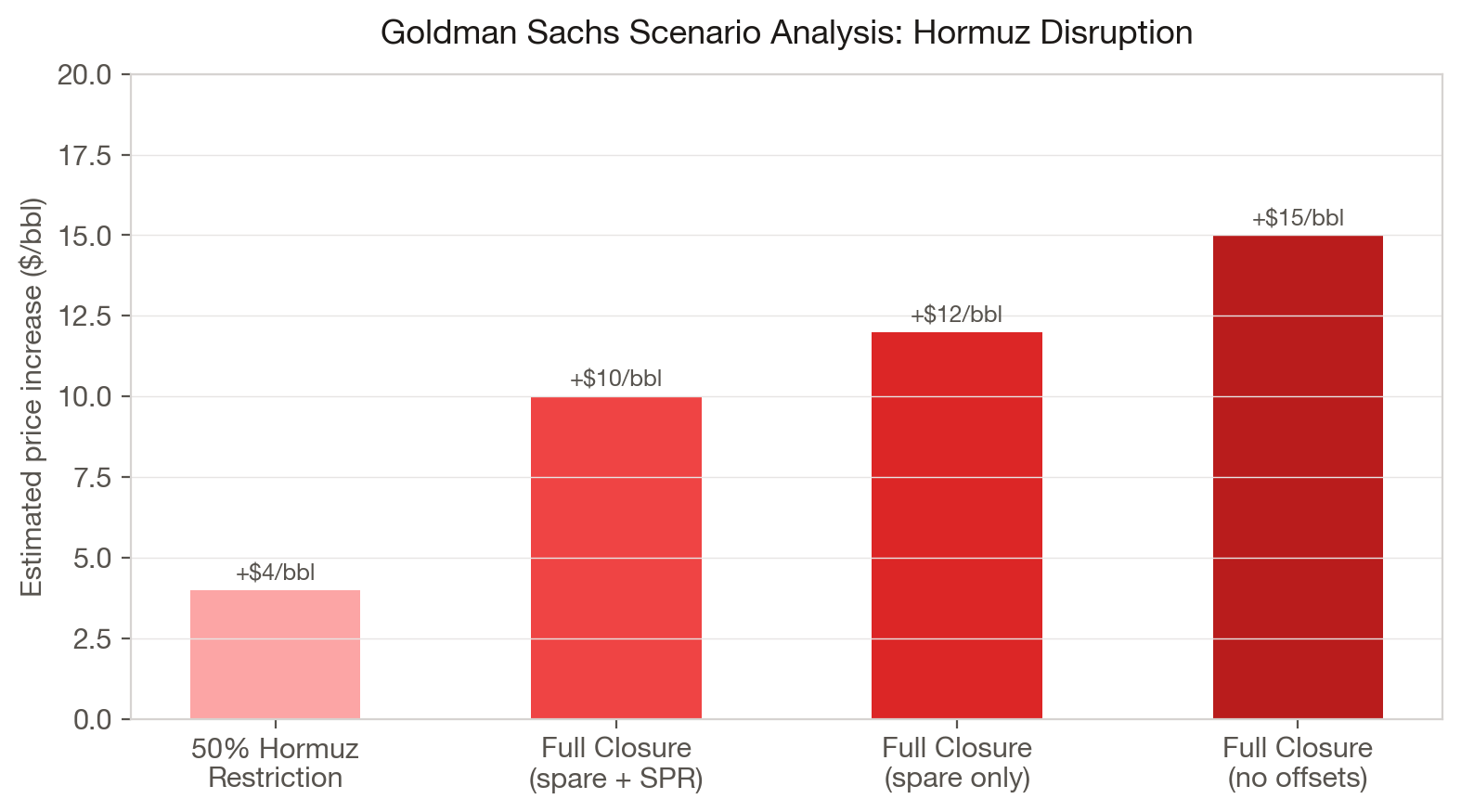

A full Hormuz closure could add $12–15/barrel to oil prices. Source: Goldman Sachs Research

Goldman Sachs models estimated a full one-month closure could add $12 to $15 per barrel to oil prices even with spare pipeline capacity and strategic reserve releases. A partial closure of 50% would add around $4. But those models assumed the disruption is temporary and contained. If it escalates, we are looking at oil well above $90, possibly approaching $100.

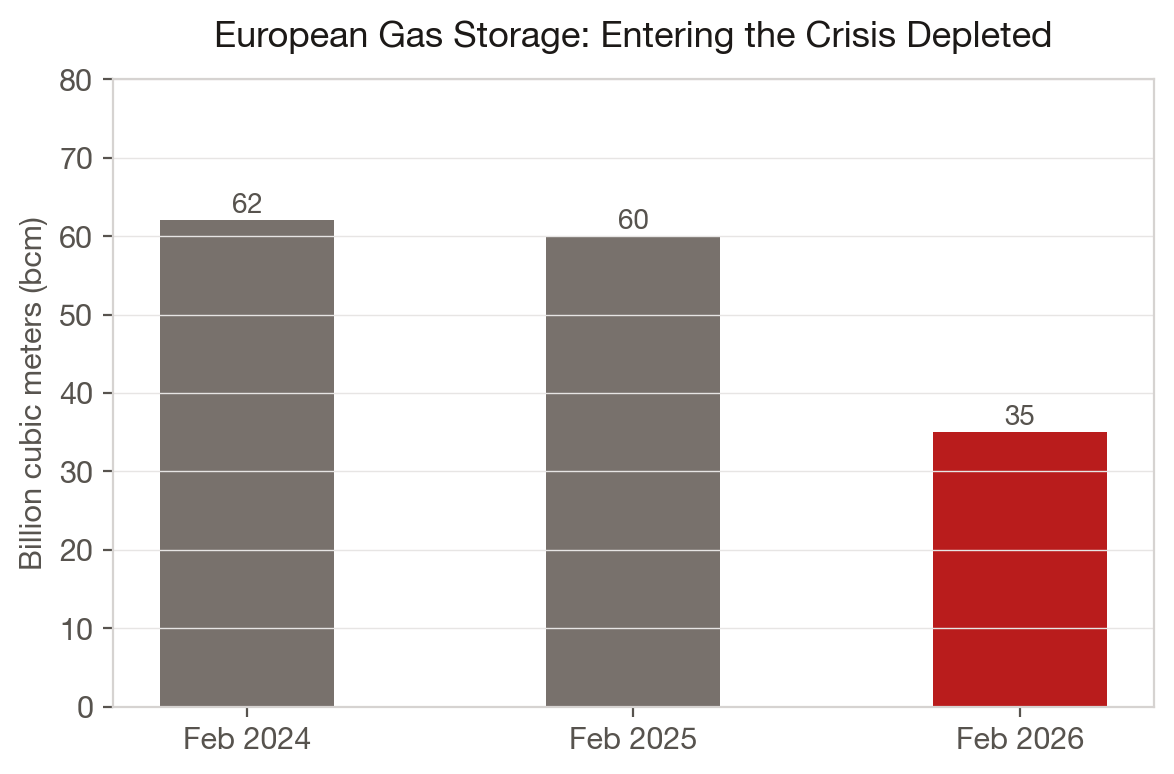

The combination of Venezuelan supply uncertainty and a potential Hormuz disruption would create a supply shock that the global economy is not priced for. European natural gas markets, already dealing with storage levels at just 33% of capacity (around 35 billion cubic meters at end of February, compared to 60 bcm a year earlier), would be especially vulnerable. LNG from Qatar, which transits the strait, accounts for about 20% of global supply.

EU gas storage at end of February 2026 was 42% below the prior year. Source: Gas Infrastructure Europe, EU Council

I want to be clear: I am not predicting that a strike will definitely happen. But the pattern is unmistakable. The same escalatory sequence that preceded Operation Midnight Hammer, a failed diplomatic track, military buildup, insurance market signals, and accelerated export behavior by the target country, is playing out again in real time. If it does happen, the energy market consequences will dwarf anything we saw from Venezuela.

Author’s note, updated March 13, 2026: Four days after this piece was published, the United States and Israel launched Operation Epic Fury on February 28, striking Iranian military facilities, nuclear sites, and leadership targets, killing Supreme Leader Ali Khamenei. Iran retaliated by attacking targets across the Gulf, including UAE and Saudi Arabia, and the IRGC declared the Strait of Hormuz closed. As of this writing, tanker traffic through the strait has effectively dropped to zero, Brent crude has surged past $100 and continues climbing (closing at $103.14 on March 13), European natural gas prices have nearly doubled, the IEA has authorized the release of 400 million barrels from global strategic reserves, and QatarEnergy has declared force majeure on its LNG exports. The specific scenario I outlined above, a Hormuz disruption creating a supply shock that cascades through oil, LNG, and fertilizer markets, has materialized almost exactly as described. The global economic impact is still unfolding.

Two interventions, two very different market reactions. Source: S&P Global Platts, CNBC, Goldman Sachs

The Bigger Picture

Step back from the headlines and the oil charts for a moment. What does all of this actually mean?

Venezuela was a test run. It was the first application of a new American strategic framework that combines military force, energy economics, and hemispheric dominance into a single, integrated approach. The Donroe Doctrine is not just rhetoric. It is being operationalized, and the Venezuela intervention demonstrated that it works, at least in the short term.

| Strategic Question | Answer | Evidence |

|---|---|---|

| Can the U.S. execute a “snatch and grab” against a sitting head of state? | Yes | Maduro captured in hours, minimal U.S. casualties |

| Will oil markets panic? | No | Brent moved +1.7% ($0.78/bbl); settled within 48 hrs |

| Will the international community impose consequences? | Not meaningfully | UN debate but no sanctions or collective action |

| Will China respond beyond rhetoric? | No | $67B invested; response limited to statements |

| Can a cooperative successor be installed quickly? | Yes | Rodríguez sworn in within days, reforms within weeks |

Those answers are transferable. They inform how Washington thinks about the next crisis, whether that is Iran, or Colombia (where Trump openly mused about a similar operation), or any other country that falls on the wrong side of American strategic interests.

The through line connecting Panama in 1989, Grenada in 1983, Iraq in 2003, Libya in 2011, and Venezuela in 2026 is not ideological. It is structural. When the United States identifies a convergence between security interests and economic opportunity (especially energy), and when the target country is militarily overmatched and diplomatically isolated, intervention becomes a question of “when” rather than “if.” The Donroe Doctrine just makes that calculus explicit in a way that previous administrations preferred to leave unsaid.

Whether this leads to stability or chaos depends entirely on execution. The historical track record is mixed at best. Panama turned out reasonably well. Libya was a disaster. Iraq falls somewhere in between, depending on your time horizon. Venezuela’s outcome is still being written, and the Iran situation could redefine the global energy landscape for years.

What I do know is this: energy markets are the scoreboard now. Follow the oil, and you will understand the geopolitics. Follow the geopolitics, and you will understand the oil.

That relationship is only going to intensify from here.

Sources: , , , , , , , , , , ,